CALGARY, ALBERTA - Aug. 8, 2012 /CNW/ - Paramount Resources Ltd. (TSX:POU)

SECOND QUARTER OVERVIEW

Oil and Gas Operations

- Average sales volumes increased 30 percent to 21,474 Boe/d in the second quarter of 2012 compared to 16,572 Boe/d in the same period in 2011; NGLs volumes increased by 31 percent.

- The Company's wholly-owned Musreau 45 MMcf/d refrigeration facility (the "Musreau Refrig Facility") has been operating near capacity since re-commissioning in March.

- Operating expenses per Boe decreased 21 percent to $8.20 from $10.40 in the second quarter of 2011 with higher Kaybob production, the re-commissioning of the Mureau Refrig Facility and the sale of higher cost US properties.

- Regulatory approval was received for the Musreau 200 MMcf/d deep cut facility and site preparation work has commenced.

- Advance drilling for the deep cut facility expansions at Musreau and Smoky continued. The Company currently has an inventory of 21 net wells with estimated first month deliverability of 34,700 Boe/d and average first year deliverability of 17,300 Boe/d.

- In May, Paramount's wholly-owned subsidiary, Summit Resources, Inc., closed the sale of all of its operated properties in North Dakota and all of its Montana properties for cash proceeds of approximately US$70 million. The Company is continuing to pursue the disposition of the remaining US properties.

Strategic Investments

- The Company is currently evaluating drilling plans for its Liard Basin Besa River shale gas lands for the 2012 / 2013 winter drilling season. Industry test results from prolific shale gas wells adjacent to Paramount's lands support the Company's internal resource estimates.

- Cavalier Energy Inc. continued to focus on finalizing its regulatory application for the first 10,000 Bbl/d phase at the Hoole property, anticipated to be submitted in the fourth quarter of 2012.

- Fox Drilling Inc. continued the construction of two new triple-sized walking drilling rigs, expected to be operational in late-2012.

Corporate

- The revolving period and maturity date of the Company's $300 million bank credit facility (the "Existing Facility") were extended to October 31, 2012 and October 31, 2013, respectively, to provide for the evaluation of an unsolicited proposal for an expanded committed credit facility (the "Proposed Facility") from one of Paramount's lenders.

- The Proposed Facility would have a term extending into 2014 and provide additional funding capacity to complete construction of the Musreau deep cut facility and to drill additional wells.

- Corporate general and administrative costs per Boe decreased 13 percent in the second quarter to $2.09 from $2.40 in 2011.

| Financial and Operating Highlights(1,2) | |||||||||||

| ($ millions, except as noted) | |||||||||||

| Three months ended June 30 | Six months ended June 30 | ||||||||||

| 2012 | 2011 | % Change | 2012 | 2011 | % Change | ||||||

| Financial | |||||||||||

| Petroleum and natural gas sales | 46.5 | 61.1 | (24) | 101.2 | 107.9 | (6) | |||||

| Funds flow from operations | 12.1 | 23.4 | (48) | 25.0 | 37.3 | (33) | |||||

| Per share - diluted ($/share) | 0.15 | 0.29 | (48) | 0.28 | 0.48 | (42) | |||||

| Net income (loss) | - | 12.2 | (100) | 124.5 | 0.3 | 100 | |||||

| Per share - basic ($/share) | - | 0.16 | (100) | 1.46 | - | 100 | |||||

| Per share - diluted ($/share)(3) | - | (0.02) | 100 | 1.43 | - | 100 | |||||

| Exploration and development expenditures | 66.4 | 54.5 | 22 | 208.6 | 214.6 | (3) | |||||

| Investments in other entities - market value(4) | 611.4 | 783.1 | (22) | ||||||||

| Total assets | 1,777.3 | 1,714.5 | 4 | ||||||||

| Net debt(5) | 472.8 | 514.1 | (8) | ||||||||

| Common shares outstanding (thousands) | 85,573 | 79,051 | 8 | ||||||||

| Operating | |||||||||||

| Sales volumes | |||||||||||

| Natural gas (MMcf/d) | 106.2 | 77.7 | 37 | 97.4 | 68.3 | 43 | |||||

| NGLs (Bbl/d) | 1,973 | 1,504 | 31 | 1,813 | 1,237 | 47 | |||||

| Oil (Bbl/d) | 1,808 | 2,110 | (14) | 2,097 | 2,231 | (6) | |||||

| Total (Boe/d) | 21,474 | 16,572 | 30 | 20,144 | 14,844 | 36 | |||||

| Average realized price | |||||||||||

| Natural gas ($/Mcf) | 2.09 | 4.36 | (52) | 2.40 | 4.26 | (44) | |||||

| NGLs ($/Bbl) | 69.63 | 81.95 | (15) | 73.71 | 79.47 | (7) | |||||

| Oil ($/Bbl) | 78.65 | 94.58 | (17) | 84.66 | 87.65 | (3) | |||||

| Net wells drilled (excluding oil sands evaluation) | 8 | 8 | - | 19 | 20 | (5) | |||||

| Net oil sands evaluation wells drilled | - | 1 | (100) | 1 | 27 | (96) | |||||

| (1) | Readers are referred to the advisories concerning non-GAAP measures and oil and gas definitions in the "Advisories" section of this document. |

| (2) | Amounts include the results of discontinued operations. Refer to pages 6 and 7 of Paramount's Management's Discussion and Analysis for the three and six months ended June 30, 2012. |

| (3) | Per share - diluted ($/share) has been adjusted for the six months ended June 30, 2011 as a result of changes to reflect discontinued operations accounting. See Paramount's unaudited Interim Condensed Consolidated Financial Statements for the three and six months ended June 30, 2012. |

| (4) | Based on the period-end closing prices of publicly traded enterprises and the book value of the remaining investments. |

| (5) | Net debt is a non-GAAP measure, it is calculated and defined in the Liquidity and Capital Resources section of Paramount's Management's Discussion and Analysis for the three and six months ended June 30, 2012. |

| REVIEW OF OPERATIONS(1) | |||||||||||

| Second Quarter 2012 |

First Quarter 2012 |

% Change | |||||||||

| Sales volumes | |||||||||||

| Natural gas (MMcf/d) | 106.2 | 88.6 | 20 | ||||||||

| NGLs (Bbl/d) | 1,973 | 1,652 | 19 | ||||||||

| Oil (Bbl/d) | 1,808 | 2,386 | (24) | ||||||||

| Total (Boe/d) | 21,474 | 18,813 | 14 | ||||||||

| Average realized prices | |||||||||||

| Natural gas ($/Mcf) | 2.09 | 2.77 | (25) | ||||||||

| NGLs ($/Bbl) | 69.63 | 78.57 | (11) | ||||||||

| Oil ($/Bbl) | 78.65 | 89.21 | (12) | ||||||||

| Total ($/Boe) | 23.82 | 31.95 | (25) | ||||||||

| Netbacks ($ millions) | ($/Boe) | ($/Boe) | % Change in $/Boe |

||||||||

| Petroleum and natural gas sales | 46.5 | 23.82 | 54.7 | 31.95 | (25) | ||||||

| Royalties | (3.9) | 2.00) | (5.3) | (3.09) | (35) | ||||||

| Operating expense and production tax | (15.9) | 8.20) | (21.3) | (12.45) | (34) | ||||||

| Transportation | (5.7) | (2.90) | (5.6) | (3.29) | (12) | ||||||

| Netback | 21.0 | 10.72 | 22.5 | 13.12 | (18) | ||||||

| Financial commodity contract settlements | 0.4 | 0.23 | (1.4) | (0.84) | 127 | ||||||

| Netback including financial commodity contract settlements | 21.4 | 10.95 | 21.1 | 12.28 | (11) | ||||||

| (1) | Amounts include the results of discontinued operations. Refer to pages 6 and 7 of Paramount's Management's Discussion and Analysis for the three and six months ended June 30, 2012. |

Paramount's sales volumes averaged 21,474 Boe/d in the second quarter of 2012 compared to 18,813 Boe/d in the first quarter, as the Musreau Refrig Facility operated near capacity after being re-commissioned in March. Valhalla production also increased following the commissioning of additional compression capacity. Second quarter NGLs sales volumes increased to 1,973 Bbl/d, including 1,200 Bbl/d of condensate.

Sales volumes in April increased to 23,000 Boe/d, the highest since Paramount spun-out Trilogy in 2005. Through May and June, throughput at the Musreau Refrig Facility was temporarily reduced to address increased liquids production from new wells brought-on through the facility. Liquids yields have since stabilized and liquids handling processes have been optimized, allowing processing levels to return to normal. Sales volumes were also impacted by the May disposition of United States properties producing approximately 900 Boe/d and by maintenance operations at a third party ethane extraction facility, which shut-in approximately 2,000 Boe/d of production at Valhalla for 15 days in May and reduced NGLs volumes in May and June.

Petroleum and natural gas sales revenue decreased by $8.2 million quarter over quarter because of a 25 percent decline in realized prices. Operating costs per Boe were 34 percent lower than in the first quarter, primarily due to the elimination of third party processing charges for volumes now processed through the Musreau Refrig Facility and higher Kaybob COU production. The sale of higher cost United States properties and higher first quarter seasonal maintenance costs in the Northern COU also contributed to the quarter over quarter decrease in operating costs.

| Kaybob |

| Second Quarter 2012 | First Quarter 2012 |

% Change | ||||||

| Sales Volumes | ||||||||

| Natural gas (MMcf/d) | 66.3 | 52.7 | 26 | |||||

| NGLs (Bbl/d) | 1,132 | 821 | 38 | |||||

| Oil (Bbl/d) | 61 | 65 | (6) | |||||

| Total (Boe/d) | 12,236 | 9,675 | 26 | |||||

| Exploration and Development Expenditures ($ millions) | ||||||||

| Exploration, drilling, completions and tie-ins | 16.9 | 40.4 | (58) | |||||

| Facilities and gathering | 23.0 | 31.1 | (26) | |||||

| 39.9 | 71.5 | (44) | ||||||

| Gross | Net | Gross | Net | |||||

| Wells Drilled | 7 | 4.7 | 6 | 4.5 | ||||

Second quarter sales volumes in the Kaybob COU averaged 12,236 Boe/d. The Musreau Refrig Facility was successfully re-commissioned in March, with Paramount's working interest share of second quarter volumes processed averaging approximately 60 percent. To date, the majority of production routed through the facility has been from horizontal Falher and earlier multi-zone Cretaceous vertical wells in which Paramount has a 50 percent working interest.

Production within the Kaybob COU remains constrained by available processing capacity, pending completion of facilities expansions at Musreau and Smoky. Paramount is working to increase its working interest share of volumes produced through available capacity by bringing on higher working interest wells. One (1.0 net) Montney formation well was brought-on production in early-August and a second 100 percent working interest well is planned to be brought-on later in the third quarter. Two (2.0 net) Montney wells are scheduled to be brought-on in the fourth quarter.

With the Musreau Refrig Facility on-stream throughout the second quarter, the Kaybob COU's operating costs decreased to approximately $5.00 per Boe, before accounting for the impact of third party processing income. The new facility provides significant savings to the Company through the elimination of third party processing fees.

Paramount submitted a $6 million insurance claim in the first quarter of 2012 related to the electrical failure at the Musreau Refrig Facility in the fourth quarter of 2011. The Company expects to receive a settlement in the second half of 2012.

Paramount received regulatory approval in July for its wholly-owned 200 MMcf/d deep cut facility at Musreau (the "Musreau Deep Cut Facility") and site preparation work has commenced. The project is proceeding on-time and on-budget and the procurement of major long lead-time equipment is complete. The Company has incurred total costs of approximately $45 million to June 30, 2012 and anticipates spending an additional $70 million during the second half of 2012. The facility is expected to be commissioned in the second half of 2013 at an estimated total cost of $180 million. The relatively minor incremental investment in deep cut facilities when compared to the cost of a similar sized refrigeration facility will add significant value to Paramount's natural gas production due to the price premium realized from the sale of additional NGLs volumes that would otherwise be sold as slightly higher heat content natural gas.

The current configuration of Company-operated Montney wells includes well site sweetening equipment and the use of chemicals to address sour gas production. Paramount has initiated a project to construct an amine processing train at the Musreau Deep Cut Facility, which will provide the capability to treat sour gas production at the plant instead of at well sites. This enhancement is expected to reduce well site equipping costs by over $1 million and reduce ongoing operating costs. The Company is currently finalizing the design of the amine train and plans to begin ordering long lead-time components later in 2012 for a planned start-up in the first half of 2014. The addition of the amine train will not impact the commissioning of the Musreau Deep Cut Facility during the second half of 2013.

Paramount is also participating in the expansion of a non-operated processing facility at Smoky (the "Smoky Deep Cut Facility"), which is being upgraded to operate as a deep cut liquids extraction plant. The Company will have a 20 percent interest in the expanded facility, up from its 10 percent share of the existing 100 MMcf/d dew point facility. The Smoky Deep Cut Facility will initially have 200 MMcf/d of raw gas capacity upon start-up, increasing to 300 MMcf/d through the later installation of an incremental 100 MMcf/d of compression. As a plant owner, Paramount has the option at any time to initiate the increase to 300 MMcf/d, which would bring the Company's total owned capacity in the plant to 60 MMcf/d. Work has commenced on the initial expansion / upgrade with orders being placed for long lead-time equipment and the establishment of a construction camp near the site.

During the second quarter, the Kaybob COU drilled four (2.7 net) Falher formation wells, two (1.0 net) Montney formation wells and one (1.0 net) directional multi-zone Cretaceous well. Three of these wells have been fracture stimulated and results have been consistent with expectations, further confirming the Company's well performance profiles. The Company has achieved lower per-well drilling costs in 2012 by optimizing drilling techniques, resulting in fewer drilling days per well, and by drilling from multi-well pads which reduces mobilization time and costs. Completion costs have also been falling as a result of lower rates for fracturing equipment.

The following table summarizes the current status of Kaybob Deep Basin wells that have been drilled and are awaiting production, the estimated remaining capital required to complete these wells, and their anticipated production and sales volumes:

| Wells | Total Remaining Capital (net) |

Estimated Net Raw Gas Production |

Estimated Net Sales Volumes(1) |

|||||||||||

| First Month | First Year | First Month | First Year | |||||||||||

| Gross | Net | ($ millions) | (MMcf/d) | (MMcf/d) | (Boe/d) | (Boe/d) | ||||||||

| Tied-in, capable of producing | 5 | 2 | - | 14 | 7 | 3,000 | 1,400 | |||||||

| Completed, awaiting tie-in | 8 | 7 | 11 | 48 | 24 | 12,500 | 6,500 | |||||||

| Drilled, awaiting completion | 16 | 12 | 65 | 80 | 38 | 19,200 | 9,400 | |||||||

| 29 | 21 | 76 | 142 | 69 | 34,700 | 17,300 | ||||||||

| (1) | Based on processing through a deep cut facility |

The Company plans to drill up to an additional 15 wells for the remainder of 2012, with more wells to be drilled in 2013 to continue building behind pipe production in advance of the completion of facilities expansions at Musreau and Smoky. Paramount continues to utilize its own facilities and third party processing capacity to maximize production while these expansions are in progress. In the interim, behind pipe wells will be produced where capacity is available.

Grande Prairie |

|||||||

| Second Quarter 2012 | First Quarter 2012 |

% Change | |||||

| Sales Volumes | |||||||

| Natural gas (MMcf/d) | 21.5 | 16.8 | 28 | ||||

| NGLs (Bbl/d) | 658 | 596 | 10 | ||||

| Oil (Bbl/d) | 269 | 391 | (31) | ||||

| Total (Boe/d) | 4,514 | 3,792 | 19 | ||||

| Exploration and Development Expenditures ($ millions) | |||||||

| Exploration, drilling, completions and tie-ins | 12.3 | 31.4 | (61) | ||||

| Facilities and gathering | 6.5 | 12.5 | (48) | ||||

| 18.8 | 43.9 | (57) | |||||

| Gross | Net | Gross | Net | ||||

| Wells Drilled | 3 | 2.1 | 5 | 3.4 | |||

Second quarter sales volumes in the Grande Prairie COU increased 19 percent to 4,514 Boe/d compared to 3,792 Boe/d in the first quarter, as additional wells were brought-on production at Valhalla following the commissioning of the gathering and compression system expansion. Sales volumes were impacted by a disruption at a downstream third party ethane extraction facility, resulting in a 15 day shut-in at Valhalla and reduced NGLs volumes in May and June. The Company was able to partially mitigate the impact of the disruption by re-routing production through alternate facilities for a portion of the outage. The third party disruption was resolved at the end of June and production has been fully restored.

The Company drilled two (2.0 net) wells at Valhalla during the second quarter and expects to complete these wells in the second half of 2012. These wells, along with an additional four (2.3 net) wells drilled in the first quarter, are expected to be brought-on production in the second half of 2012.

At Karr-Gold Creek, surface equipment that had been ordered as part of a well performance enhancement program was delivered and installed on two (2.0 net) wells that had previously been completed but not placed on production. The wells were brought-on in April and the Company is continuing to evaluate the results.

Southern |

| Second Quarter 2012 |

First Quarter 2012 |

% Change | |||||

| Sales Volumes(1) | |||||||

| Natural gas (MMcf/d) | 9.8 | 11.0 | (11) | ||||

| NGLs (Bbl/d) | 169 | 217 | (22) | ||||

| Oil (Bbl/d) | 1,250 | 1,663 | (25) | ||||

| Total (Boe/d) | 3,059 | 3,718 | (18) | ||||

| Exploration and Development Expenditures(1) ($ millions) | |||||||

| Exploration, drilling, completions and tie-ins | 1.9 | 4.4 | (57) | ||||

| Facilities and gathering | 0.7 | 1.4 | (50) | ||||

| 2.6 | 5.8 | (55) | |||||

| Gross | Net | Gross | Net | ||||

| Wells Drilled | - | - | 1 | 0.5 | |||

| (1) | Amounts include the results of discontinued operations. Refer to page 6 and 7 of Paramount's Management's Discussion and Analysis for the three and six months ended June 30, 2012. |

In May 2012, Paramount's wholly-owned subsidiary, Summit Resources, Inc. ("Summit"), closed the sale of all of its operated properties in North Dakota and all of its Montana properties for cash proceeds of approximately US$70 million. The disposition included approximately 900 Boe/d of production and approximately 38,000 (27,000 net) acres of land.

The transaction did not include Summit's Bakken / Three Forks lands in North Dakota with production of approximately 200 Boe/d and joint venture exploratory acreage. The Company is continuing to pursue the disposition of the remaining US properties.

Second quarter sales volumes in the Southern COU decreased mainly because of the US property disposition.

The Southern COU plans to drill three (2.5 net) wells in Harmattan in Southern Alberta during the second half of 2012 targeting liquids-rich natural gas.

Northern |

|||||||

| Second Quarter 2012 |

First Quarter 2012 |

% Change | |||||

| Sales Volumes | |||||||

| Natural gas (MMcf/d) | 8.6 | 8.1 | 6 | ||||

| NGLs (Bbl/d) | 14 | 18 | (22) | ||||

| Oil (Bbl/d) | 228 | 267 | (15) | ||||

| Total (Boe/d) | 1,665 | 1,628 | 2 | ||||

| Exploration and Development Expenditures ($ millions) | |||||||

| Exploration, drilling, completions and tie-ins | 0.6 | 18.5 | (97) | ||||

| Facilities and gathering | 1.9 | 2.3 | (17) | ||||

| 2.5 | 20.8 | (88) | |||||

| Gross | Net | Gross | Net | ||||

| Wells Drilled | - | - | 2 | 2.0 | |||

Second quarter sales volumes in the Northern COU were unchanged from the first quarter of 2012. Processing disruptions at the Bistcho plant impacted second quarter volumes.

Paramount's first well at Birch in Northeast British Columbia was brought-on production in the second quarter and subsequently shut-in due to higher than expected liquids production. Modifications to surface equipment are underway and the well is expected to be re-started in the third quarter. The Company has 3 MMcf/d of raw gas processing capacity at Birch and will bring on two (2.0 net) additional wells as production from the initial well moderates. Production results from these wells will be evaluated over the coming months.

STRATEGIC INVESTMENTS

Cavalier Energy Inc. ("Cavalier") continued to build its management team during the second quarter of 2012. The team's efforts are focused on finalizing the regulatory application for the first phase of development at the Hoole property, a 10,000 Bbl/d project targeting the Grand Rapids formation using proven SAGD technologies. Cavalier remains on schedule to submit this application in the fourth quarter of 2012 and anticipates first steam commencing as early as the second half of 2015. Longer-term plans for Hoole include three additional 30,000 Bbl/d phases that would increase production to 100,000 Bbl/d by 2024.

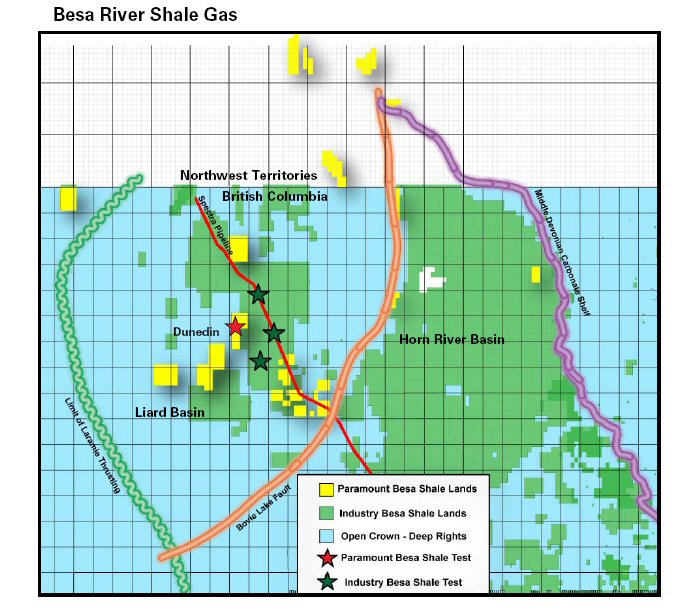

SHALE GAS

Paramount's Besa River shale gas holdings are focused in the Liard Basin in Northeast British Columbia and the Northwest Territories. The Company began drilling a vertical evaluation well at a winter access location at Dunedin in the first quarter before suspending operations due to warm weather. Paramount is evaluating further drilling plans for its shale gas lands for the 2012 / 2013 winter drilling season. Recently announced industry test results from prolific shale gas wells adjacent to Paramount's lands support the Company's internal estimates of the resource.

To view the Besa River Shale Gas map, please visit the following link: image/2012+Aug+8+image.jpg.

CORPORATE

In the course of renewing its $300 million Existing Facility in the second quarter, the Company received an unsolicited proposal from one of its lenders to provide an expanded committed credit facility that would replace the Existing Facility.

The Proposed Facility would have a term extending into 2014 and provide additional funding capacity to complete construction of the Musreau deep cut facility and to drill additional wells.

In order to provide sufficient time for Paramount and its lenders to perform due diligence and negotiate the terms of the Proposed Facility, the revolving period and maturity date of the Existing Facility were extended to October 31, 2012 and October 31, 2013, respectively. All other terms of the Existing Facility remain unchanged.

OUTLOOK

Paramount's annual 2012 capital spending budget (excluding land, acquisitions and capitalized interest) remains at $535 million, with $475 million allocated to exploration and development spending in the Company's core producing areas and $60 million allocated to Strategic Investment spending. The Company has more than sufficient capacity to fund its 2012 capital program with its Existing Facility and retains flexibility within its current capital plan to vary spending depending upon future economic conditions, among other factors.

Year-to-date exploration and development spending is approximately $210 million. Planned spending of $265 million for the remainder of the year will be focused in the Kaybob Deep Basin development, where $85 million will be invested in the Musreau and Smoky deep cut facilities and drilling will continue in order to build an inventory of wells to feed the expansions. By year-end 2012, Paramount expects to have an inventory of approximately 34 wells awaiting the commissioning of these new facilities.

Strategic Investment spending for the remainder of the year will be directed to completing the construction of two walking drilling rigs.

Sales volumes are expected to increase during the remainder of the year as new wells are brought-on production and Paramount's working interest share of volumes produced through available capacity in the Kaybob COU increases. The Company expects its 2012 exit rate will be approximately 26,000 Boe/d and that sales volumes thereafter will range between 25,000 Boe/d and 27,000 Boe/d until the Musreau Deep Cut Facility is fully commissioned in the second half of 2013. Sales volumes are expected to more than double once the Musreau Deep Cut Facility and the Smoky Deep Cut Facility are fully operational in 2014.

ADDITIONAL INFORMATION

A copy of Paramount's complete results for the three and six months ended June 30, 2012, including Management's Discussion and Analysis and the unaudited Interim Condensed Consolidated Financial Statements for the three and six months ended June 30, 2012 can be found at download/2012+Aug+8.pdf. This information will also be made available through Paramount's website at www.paramountres.com and SEDAR at www.sedar.com.

ABOUT PARAMOUNT

Paramount Resources Ltd. is a Canadian oil and natural gas exploration, development and production company with operations focused in Western Canada. Paramount's common shares are listed on the Toronto Stock Exchange under the symbol "POU".

ADVISORIES

FORWARD-LOOKING INFORMATION

Certain statements in this document constitute forward-looking information under applicable securities legislation. Forward-looking information typically contains statements with words such as "anticipate", "believe", "estimate", "expect", "plan", "intend", "propose", or similar words suggesting future outcomes or an outlook. Forward looking information in this document includes, but is not limited to:

- expected production and sales volumes and the timing thereof;

- planned exploration and development expenditures and strategic investment expenditures and the timing thereof;

- exploration and development potential, plans and strategies and the anticipated costs, timing and results thereof;

- budget allocations and capital spending flexibility;

- availability of facilities to process and transport natural gas production;

- the anticipated costs, scope and timing of proposed new facilities and expansions to existing facilities and the expected capacity and utilization of such facilities;

- the anticipated incremental benefit provided by a deep cut facility over a refrigeration facility;

- the timing of the anticipated development of Paramount's oil sands, carbonate bitumen and shale gas assets;

- ability to fulfill future pipeline transportation commitments;

- the anticipated costs and completion date of the two new triple-sized walking drilling rigs;

- business strategies and objectives;

- sources of and plans for financing;

- the outcome of diligence reviews and negotiations concerning the Proposed Facility, including the size, timing and terms thereof;

- acquisition and disposition plans;

- operating and other costs;

- regulatory applications and the anticipated scope, timing and results thereof;

- expected drilling programs, completions, well tie-ins, facilities construction and expansions and the timing thereof; and

- the outcome and timing of any legal claims, insurance claims, audits, assessments, regulatory matters and proceedings.

Such forward-looking information is based on a number of assumptions which may prove to be incorrect. The following assumptions have been made, in addition to any other assumptions identified in this document:

- future crude oil, bitumen, natural gas and NGLs prices and general economic, business and market conditions;

- the ability of Paramount to obtain required capital to finance its exploration and development activities;

- the ability of Paramount to obtain equipment, services, supplies and personnel in a timely manner and at an acceptable cost to carry out its activities;

- the ability of Paramount to market its oil, natural gas and NGLs successfully to current and new customers;

- the ability of Paramount to close expected property sales and the timing thereof;

- the ability of Paramount to secure adequate product processing, transportation and storage;

- the ability of Paramount and its industry partners to obtain drilling success consistent with expectations, including liquids yields;

- the timely receipt of required regulatory approvals;

- expected timelines being met in respect of facility development and construction projects;

- access to capital markets and other sources of funding;

- well economics relative to other projects; and

- currency exchange and interest rates.

Although Paramount believes that the expectations reflected in such forward looking information is reasonable, undue reliance should not be placed on it as Paramount can give no assurance that such expectations will prove to be correct. Forward-looking information is based on current expectations, estimates and projections that involve a number of risks and uncertainties which could cause actual results to differ materially from those anticipated by Paramount and described in the forward looking information. These risks and uncertainties include, but are not limited to:

- fluctuations in crude oil, bitumen, natural gas and NGLs prices, foreign currency exchange rates and interest rates;

- the uncertainty of estimates and projections relating to future revenue, future production, liquids yields, costs and expenses and the timing thereof;

- the ability to secure adequate product processing, transportation and storage;

- the uncertainty of exploration, development and drilling activities;

- operational risks in exploring for, developing and producing crude oil and natural gas, and the timing thereof;

- the ability to obtain equipment, services, supplies and personnel in a timely manner and at an acceptable cost;

- potential disruptions or unexpected technical difficulties in designing, developing or operating new, expanded or existing facilities including third party facilities;

- risks and uncertainties involving the geology of oil and gas deposits;

- the uncertainty of reserves and resource estimates;

- the ability to generate sufficient cash flow from operations and other sources of financing at an acceptable cost to fund exploration, development and operational activities and meet current and future obligations, including costs of anticipated projects;

- changes to the status or interpretation of laws, regulations or policies;

- changes in environmental laws including emission reduction obligations;

- the receipt, timing, and scope of governmental or regulatory approvals;

- changes in economic, business and market conditions;

- uncertainty regarding aboriginal land claims and co-existing with local populations;

- the effects of weather;

- the timing and cost of future abandonment and reclamation activities;

- cleanup costs or business interruptions due to environmental damage and contamination;

- the ability to enter into or continue leases;

- existing and potential lawsuits and regulatory actions; and

- other risks and uncertainties described elsewhere in this document and in Paramount's other filings with Canadian securities authorities, including its Annual Information Form.

The foregoing list of risks is not exhaustive. Additional information concerning these and other factors which could impact Paramount are included in Paramount's most recent Annual Information Form. The forward-looking information contained in this document is made as of the date hereof and, except as required by applicable securities law, Paramount undertakes no obligation to update publicly or revise any forward-looking statements or information, whether as a result of new information, future events or otherwise.

NON-GAAP MEASURES

In this document "Funds flow from operations", "Funds flow from operations per share - diluted", "Netback", "Netback including financial commodity contract settlements", "Net Debt", "Exploration and development expenditures" and "Investments in other entities - market value", collectively the "Non-GAAP measures", are used and do not have any standardized meanings as prescribed by Generally Accepted Accounting Principles in Canada ("GAAP").

Funds flow from operations refers to cash from operating activities before net changes in operating non-cash working capital, geological and geophysical expenses and asset retirement obligation settlements. Funds flow from operations is commonly used in the oil and gas industry to assist management and investors in measuring the Company's ability to fund capital programs and meet financial obligations.

Netback equals petroleum and natural gas sales less royalties, operating costs, production taxes and transportation costs. Netback is commonly used by management and investors to compare the results of the Company's oil and gas operations between periods. Net Debt is a measure of the Company's overall debt position after adjusting for certain working capital amounts and is used by management to assess the Company's overall leverage position. Refer to the calculation of Net Debt in the liquidity and capital resources section of Management's Discussion and Analysis. Exploration and development expenditures refer to capital expenditures and geological and geophysical costs incurred by the Company's COUs (excluding land and acquisitions). The exploration and development expenditure measure provides management and investors with information regarding the Company's Principal Property spending on drilling and infrastructure projects, separate from land acquisition activity.

Investments in other entities - market value reflects the Company's investments in enterprises whose securities trade on a public stock exchange at their period end closing price (e.g. Trilogy, MEG Energy, MGM Energy and others), and investments in all other entities at book value. Paramount provides this information because the market values of equity-accounted investments, which are significant assets of the Company, are often materially different than their carrying values.

Non-GAAP measures should not be considered in isolation or construed as alternatives to their most directly comparable measure calculated in accordance with GAAP, or other measures of financial performance calculated in accordance with GAAP. The Non-GAAP measures are unlikely to be comparable to similar measures presented by other issuers.

OIL AND GAS MEASURES AND DEFINITIONS

This document contains disclosures expressed as "Boe", "Boe/d" and "$/Boe". All oil and natural gas equivalency volumes have been derived using the ratio of six thousand cubic feet of natural gas to one barrel of oil. Equivalency measures may be misleading, particularly if used in isolation. A conversion ratio of six thousand cubic feet of natural gas to one barrel of oil is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the well head. The term "liquids" is used to represent oil and natural gas liquids.

During the second quarter of 2012, the value ratio between crude oil and natural gas was approximately 38:1. This value ratio is significantly different from the energy equivalency ratio of 6:1. Using a 6:1 ratio would be misleading as an indication of value.

{kind=link}